At times, being helpful is the least helpful thing we can do.

As human beings, we have a natural tendency to want to help others. When we see another person dealing with challenges, we want to give them solutions. “If they’d just do what I tell them to do, all would be better.”

On the other hand, if you are like me and most others I know, you would have experienced that giving solutions don’t work. I wrote about this in an earlier article. https://josephkuosmusings.com/2020/05/05/moving-mountains/

So what do I do? In recent years, I’ve become a strong believer and supporter of Motivational Interviewing (MI). For those not familiar, MI is a conversation style developed to support people who are ambivalent.

When I am ambivalent—when I say I want one thing but do another—it is usually not because I lack some critical information. Being ambivalent means that I see both upside and downside to the decision I am making. The arguments between changing or not changing have been raging in my head for quite some time.

So what happens when someone else steps in and tells me to change? Chances are, I’ve already considered most of what the other person is saying. The conversation becomes one where I defend myself and play devil’s advocate. As I articulate why I cannot change, I become even more cemented in the status quo.

For example, someone who has smoked for decades probably already knows a lot about the negative consequences of smoking. The fact that this person is still smoking means that he/she 1) sees the upside of smoking and 2) sees the downside of quitting. Without a compelling reason to change, the status quo wins. If I start telling this person all the benefits they already know about quitting, I invite all the reasons they don’t quit. There is a natural human tendency to avoid being wrong. In effect, I force them to justify their decision and double down.

The effort to fix me becomes my fuel to stay the same.

Motivational Interviewing takes a different approach. It is not reverse psychology. As a practitioner, I neither argue for or against the change or the status quo. Instead, I partner with the person seeking help and accept this person where they are.

I trust that within all of us is the wisdom that knows what’s best for us. Despite any blind spots you may have about yourself, you are still the world’s authority on you. In this partnership, I bring expertise from my domain and you bring your expertise on yourself. Throughout the MI process, we collaborate to bring forth your own motivation for change and what you will do for yourself. So what do I do?

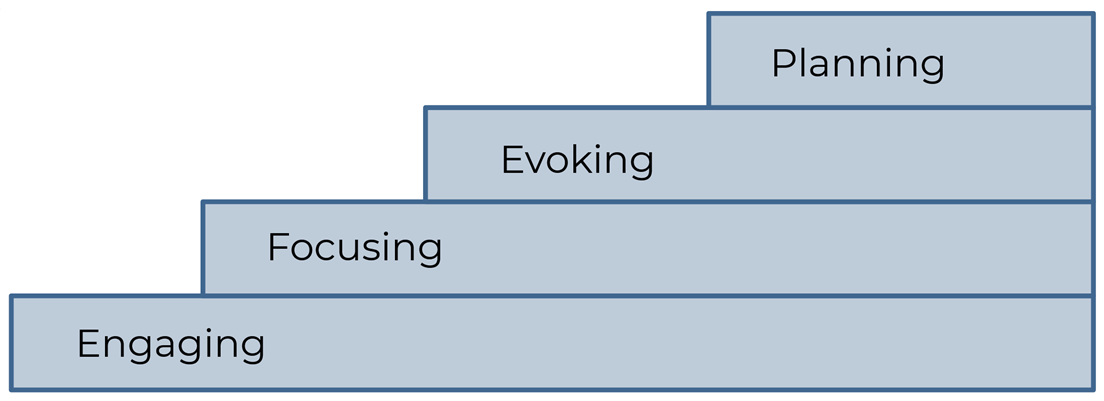

Steps of Motivational Interviewing

The MI process starts with Engaging. With this first step, I’m seeking to build rapport with the other person (my “client”). This is the foundation of all the other steps. In fact, this never stops. If my client and I are struggling with any of the other steps, we come back to Engaging.

Engaging is about establishing a partnership with my client. My focus is on understanding the client’s views and perspectives. This does not mean that I agree or condone. It means that I do my best to appreciate that my client’s perspectives are as real as my own.

This can be very difficult! When I hear something I don’t agree with, it’s natural to want to “fix” it. Such as when a client wants to retire at 55 while spending a large proportion of her income eating out. Or when a couple worries about paying for their kids’ education while buying an expensive car.

The fixing may look like informing, consoling, arguing, correcting, advising. In effect, I am saying, “well, here’s what I think…” When I am fixing, I’ve transformed the conversation to be about me rather than about them. Instead, I listen for what the client is wanting to be known for and their needs underneath.

The client who eats out a lot is in a stressful job. Eating out is a way for her to decompress. We realized that no plan can work for her without incorporating a way for her to relax.

The couple is buying an expensive car because it’s much better for the environment. To contribute to future generations, they are willing to reprioritize what’s important for them.

Finally, when I have a good idea what the client is saying, I share what I hear back to the client. I ask him/her to correct what I said or add to it. In this way, I not only listened, I demonstrated my understanding.

Genuine interest, acceptance, and demonstration of understanding are elements that build rapport.

Once I have a better understanding of the client’s world, we can narrow our focus to a topic. The idea is to have enough trust so that we can go deep while minimizing defensiveness.

The process of focusing is inviting the client to decide what they are willing to discuss. This honors the autonomy of the client and encourages buy-in. I need to trust that the topic the client selects is the most important item they are willing to work on. This is especially true when I have a different perspective on what the client SHOULD talk about. As you might imagine, clients will start resisting if they feel manipulated or forced.

Since I am a financial life planner, most of my clients want to talk about something finance-related. This might be implementing an automatic savings plan, investing in the stock market, or deciding to buy a house.

Clients decide the focus of the conversation rather than being forced to participate.

Once the topic for discussion has been decided, we move to the evoking process. This is the component that differentiates MI from other conversational styles. There is a “guiding” aspect to MI; a direction that the client wants to go, such as exercise more, eat healthier, save more, etc.

However, I’m not in the role of cheerleader or teacher. Instead, I collaborate with the client to uncover why this goal is so important.

Because the client is ambivalent (or the goal would have been achieved already) this is not straightforward. The MI conversation is a dance. A dance that shifts our collective attention from what’s keeping the client in place, to what gets the client moving.

This is a dance because the client will bring up reasons for both changing and not changing. I cannot force the client to change, so I sway with the tempo while I guide.

When the client speaks, I very deliberately choose what I reflect back and what I do not.

This guiding is not manipulation; the client already has the desire to change within. Rather, I advocate for the strength within the client. By reflecting the client’s motivation for change and softening the reasons he/she is stuck, I help sweep the debris out of the client’s way.

For example, I have a client who is struggling with implementing a savings plan. In conversations with him, I listen for his own words that demonstrated:

- Characteristics that would help him succeed, such as dedication, willpower and strength.

- Past achievements that are similar to what he needs to accomplish now.

- What he would gain in the future with such a plan and why that result is important.

Then, I reflect these gems back to him and help him hear what I heard. Through this process, clients gain more clarity on their “whys” and find their own motivation to keep going.

When the client is clear about the “what” and “why”, we start the planning process.

The transition from evoking to planning is very delicate. If I move too fast, the client will resist and we go back to re-engaging for rapport. If I move too slow, the client loses momentum and we miss an opportunity for authentic commitment.

To gauge whether the client is ready, I might propose a hypothetical scenario for the client to consider, or just ask directly. Once the client agrees, we can start working on an action plan.

This is where my financial expertise and experience come in. With the client’s permission, I can provide information, advise, and give options. One key point, however, is that the client continues to have autonomy.

The client chooses what he/she will implement.

At the end of the day, the plan must be the client’s plan. They design their plan for their own reasons. If the client feels that the plan is mine and they are following it because of me, the plan will likely fail quickly.

For the client who is establishing a savings plan, he decides how much and how often he will contribute to his savings. While I can give him recommendations on what he needs for his goals or what others have done, he is ultimately responsible for his own life.

This is a high level overview of Motivational Interviewing. The actual practice of MI is subtle and intricate, but I hope this gives you a good idea of what it is and why it’s so powerful.